This morning, while the country was watching the public back-and-forth between the Office of the Prime Minister and EyeWitness News over the status of the Grand Lucayan deal, another set of documents quietly demands attention — the energy reform agreements involving Bahamas Power and Light (BPL).

Now, I’m not saying anything is wrong. Not at all. I’m just asking questions. You see, sometimes the details tell you more than the headlines do.

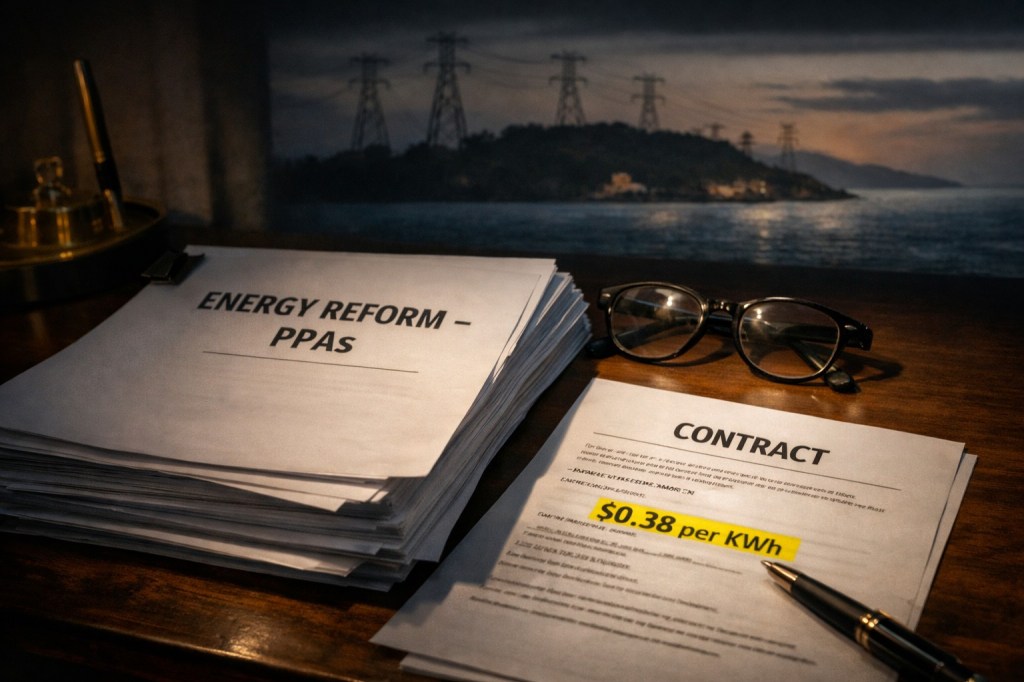

According to reporting by The Nassau Guardian, the Davis administration released more than 3,000 pages of energy reform agreements outlining Power Purchase Agreements (PPAs) between BPL and several private companies. These companies will build, own, and operate solar and LNG generation facilities on Family Islands, and BPL will purchase electricity from them at contracted rates.

The government describes this as a “sweeping energy reform effort” designed to “right-size” BPL and modernize operations at a utility that has faced long-standing financial challenges.

Now that word — “right-size.” I wonder. What exactly does that mean?

Does it mean reducing BPL’s generation footprint?

Does it mean shifting risk to private operators?

Does it mean downsizing staff?

Or does it simply mean transferring generation assets into private hands while BPL becomes primarily a purchaser and distributor?

Because under these PPAs, BPL does not own the new plants. The private entities do. They build them. They operate them. They own them.

One of the disclosed agreements involves Andros Renewable Energy Co., which proposes:

- Central Andros: 0.4 MW solar + 2 MW LNG

- North Andros: 0.4 MW solar + 2 MW LNG

- South Andros: 0.2 MW solar + 1.6 MW LNG

That totals 1 MW of solar and 5.6 MW of LNG.

Now, forgive me, but when something is described as renewable reform, and the overwhelming capacity is LNG — that’s still imported fossil fuel — one has to ask: is this diversification or substitution?

The LNG for these plants is to be supplied from a terminal at Clifton Pier, developed by Freeport Oil Company Ltd. in partnership with Shell North America.

Which raises another gentle question: how much of this structure represents true Bahamian ownership and control? If generation, fuel supply, and logistics are concentrated among a small group of external partners, where exactly does long-term energy sovereignty rest?

Let’s talk pricing.

BPL is to pay:

- 25 cents per kWh (base rate)

- 13 cents per kWh (LNG logistics)

Total: 38 cents per kWh.

Now, Deputy Director of Energy Verron Darville reportedly stated that it costs BPL more than that to currently generate power in Andros and that Family Island losses amount to roughly $50 million annually — subsidized by New Providence operations.

If that is accurate, then 38 cents could indeed represent a reduction in BPL’s internal generation cost.

But here’s the quiet part.

38 cents is what BPL pays the generator.

Consumers pay:

- Generation

- Transmission

- Distribution

- Administrative overhead

- Fuel surcharge adjustments

So one might wonder: after BPL’s additional costs are layered in, what does the final consumer rate look like? The government says there is no change to the national pricing structure. But over 15- to 25-year PPA terms — which are typical for such agreements — how will adjustment clauses affect pricing?

Because some components of these contracts are:

- Variable

- Subject to annual adjustments

- Not yet fully determined

And LNG pricing, as we know, is tied to global markets.

If LNG prices spike, who bears that risk?

Is it the generator?

Is it BPL?

Or is it the Bahamian ratepayer?

And if the logistics portion — 13 cents per kWh — is adjustable, what mechanisms cap that exposure?

Then there is the logistical dependency.

All LNG originates from Clifton Pier on New Providence and must be transported to Andros. That introduces:

- Supply chain vulnerability

- Weather exposure

- Terminal performance risk

If there is disruption at the LNG terminal or in marine transport, what redundancy exists for Family Island supply?

Now, let’s be clear.

If these agreements are well structured:

- Family Island losses could shrink.

- Government subsidies could decline.

- BPL’s balance sheet could stabilize.

- Diesel dependence could decrease.

- Emissions could improve relative to heavy fuel oil.

That is the optimistic case.

But if pricing assumptions are miscalculated, or escalation clauses are too generous, The Bahamas could be locked into long-term payment obligations — even if future solar and battery storage technologies become cheaper.

That is the structural risk inherent in long-term PPAs.

So perhaps the real issue isn’t whether 38 cents sounds high.

The real questions might be:

- Is 38 cents materially lower than BPL’s fully loaded current production cost?

- What is the exact PPA term length?

- What are the escalation formulas?

- Who bears fuel price volatility?

- What are the termination or buyout clauses?

- How much Bahamian equity participation exists?

- What independent cost benchmarking was done before signing?

Because without full clarity on those points, it becomes difficult to determine whether this is transformative reform — or simply the relocation of financial risk from one column of the national ledger to another.

I’m not suggesting anything, you understand.

I’m just asking.

Because when a nation signs decades-long energy contracts, it’s not merely buying electricity.

It’s defining its economic structure, its fiscal exposure, and its sovereignty over a system every Bahamian household depends upon.

So, these are my thoughts on the Energy Reform initiative as proposed by the New Day Progressive Liberal Party (PLP) government and elevation of them.

END